plan the life after work

Retirement Planning

Ready to Turn Your Portfolio Into Retirement Income?

Reaching retirement is one milestone—structuring reliable income for the decades that follow is another. Many investors discover that portfolio balances alone don’t answer questions about withdrawal timing, Social Security decisions, or long-term tax exposure. Ascent Financial Group provides retirement income planning designed to coordinate withdrawals, tax strategy, and investment management into one framework. The goal is to replace uncertainty with a structured retirement income plan.

Approaching Retirement With Multiple Accounts

If your savings are spread across 401(k)s, IRAs, brokerage accounts, and employer plans, withdrawal sequencing becomes complex. A coordinated strategy ensures each account supports long-term income stability.

Planning Around Equity Compensation

Stock options, RSUs, and deferred compensation plans often affect retirement timing and tax exposure. Planning helps evaluate diversification, vesting schedules, and liquidity events before retirement begins.

Transitioning From Accumulation to Income

The shift from saving to spending requires a new investment strategy. Portfolio allocations often evolve to balance income stability, growth, and longevity risk.

Managing Required Minimum Distributions (RMDs)

Once RMDs begin, tax planning becomes even more important. Coordinating distributions with charitable giving strategies, Roth conversions, and tax brackets helps reduce long-term drag.

need an example?

Get a look at a sample financial snapshot!

How It Works

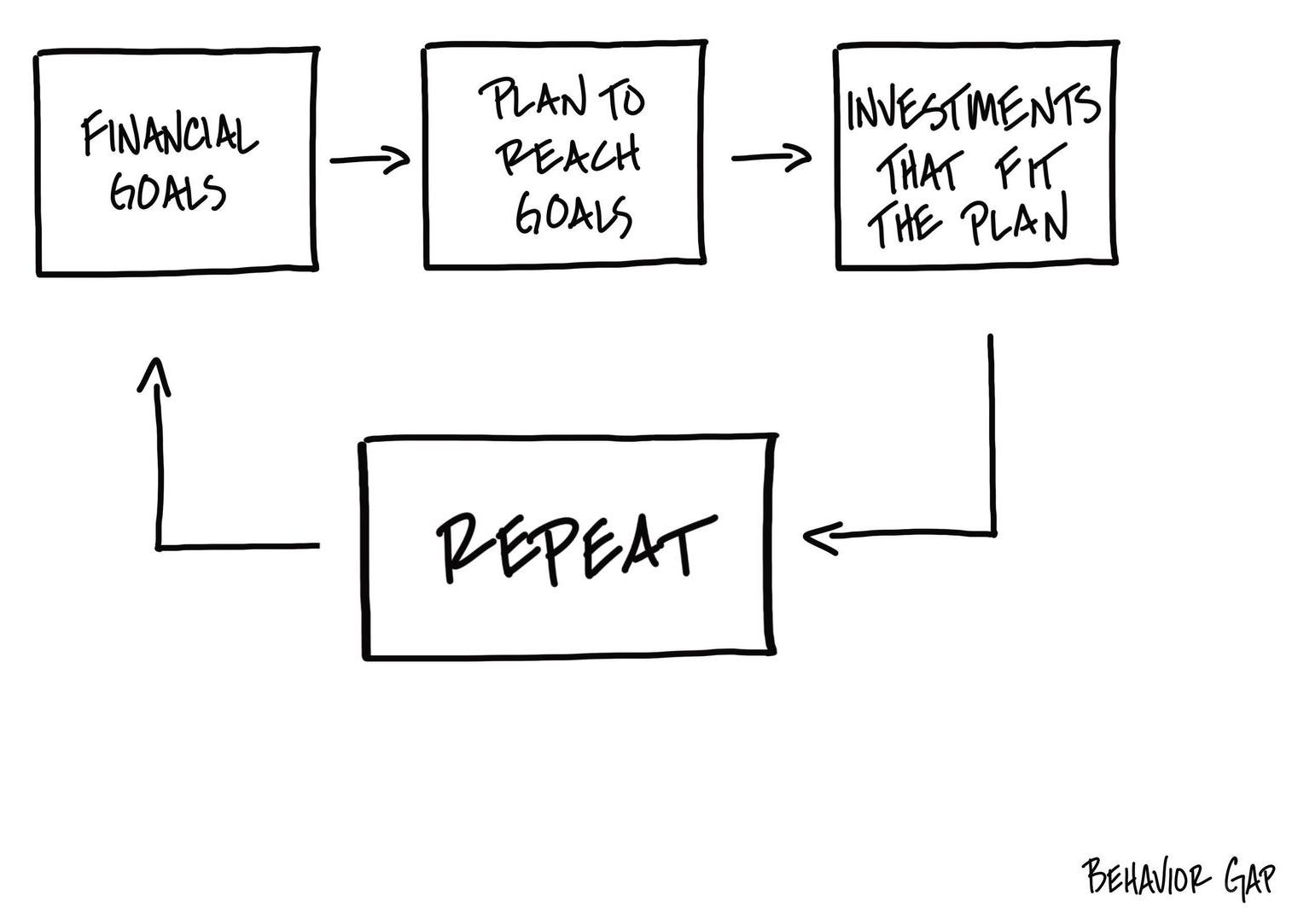

You likely have several financial planning pieces in place—you pay taxes, invest at least a portion of your savings, have some insurance, and maybe you have done some estate planning and retirement planning, but chances are each of these pieces was developed independently and at different times in your life.

To be effective, financial planning needs to be coordinated.

Each piece of the financial plan needs to accomplish its own specific tasks as well as support the tasks of each other piece.

We help make a plan that makes sense of all the moving parts. Whether you are planning for a second home, a new adventure, or retirement, we can help you make smart choices — and work toward getting there faster.

What You Receive From Retirement Income Planning

Clients working with Ascent Financial Group receive a structured retirement planning framework that includes:

Long-term retirement income projections

Withdrawal and distribution strategy design

Social Security timing analysis

Required Minimum Distribution (RMD) planning

Tax-efficient withdrawal sequencing

Coordination with broader wealth strategy

frequently asked questions about retirement planning

How early should I start retirement planning?

The short answer: as early as possible. Starting sooner gives your money more time to grow through compounding, which can make a meaningful difference over time. Even small contributions early in your career can add up significantly.

That said, it’s never too late to start. Whether you’re just beginning or getting closer to retirement, the key is having a plan that aligns with your goals, timeline, and lifestyle. As your career and life evolve, your retirement strategy should evolve with it—through regular reviews and adjustments.

What is a retirement income strategy?

A retirement income strategy is a plan for turning your savings into a reliable, tax-efficient stream of income once you stop working. Instead of focusing on growing your portfolio, the goal shifts to generating income that can support your lifestyle throughout retirement.

This includes deciding when to draw from different accounts (like taxable, retirement, and Roth accounts), how to incorporate sources like Social Security, and how to manage taxes and market risk along the way. A thoughtful strategy helps ensure your money lasts, even through market ups and downs, while giving you confidence in how and when to spend.

Can retirement planning reduce taxes?

Yes—thoughtful retirement planning can play a significant role in reducing your lifetime tax burden. By strategically choosing when and how to withdraw from different accounts (such as taxable, tax-deferred, and Roth accounts), you can potentially minimize the taxes you pay over time.

Strategies may include things like Roth conversions, tax-efficient withdrawal sequencing, and managing income to stay within favorable tax brackets. The goal isn’t just to grow your savings, but to keep more of what you’ve earned by being intentional about taxes both before and during retirement.