keep more of what you earn

Tax Planning

Are Your Financial Decisions Creating Unnecessary Taxes?

High-income professionals often make major financial decisions—investment sales, equity exercises, retirement withdrawals—without seeing the full tax impact until months later. Reactive tax preparation can leave valuable planning opportunities on the table. Ascent Financial Group provides year-round tax planning for high earners designed to coordinate investments, retirement strategy, and income planning. For clients in Richmond and across Central Virginia, the focus is proactive planning that keeps taxes aligned with long-term financial goals.

Managing Taxes on Equity Compensation

RSUs, stock options, and deferred compensation plans often create unpredictable tax exposure. Coordinated planning helps evaluate exercise timing, withholding gaps, and diversification decisions.

Reducing Taxes on Retirement Income

Retirement withdrawals can trigger significant tax consequences if not planned carefully. Coordinated strategies help evaluate Roth conversions, withdrawal sequencing, and tax bracket management.

Handling Irregular Income

Bonuses, equity vesting, and liquidity events can create uneven income patterns. Year-round tax planning helps align estimated payments and withholding strategies with real income timing.

Integrating Charitable Giving

Charitable strategies such as donor-advised funds or qualified charitable distributions can align philanthropic goals with tax planning considerations.

need an example?

Get a look at a sample Tax Review!

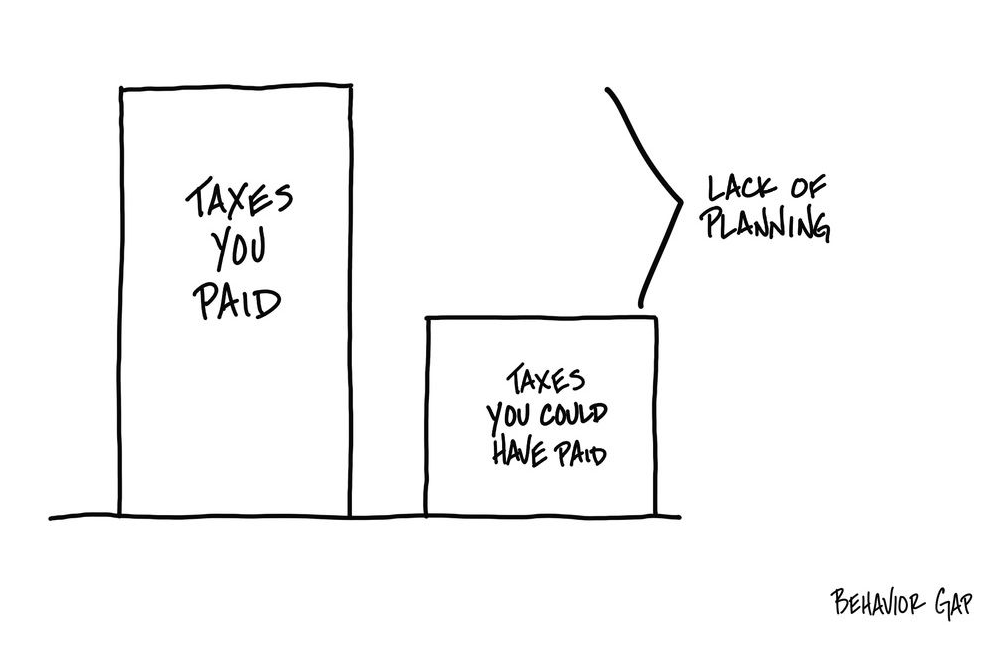

Maximizing Wealth Through a Personalized Tax Plan

A personalized tax plan is essential to helping you keep more of what you earn and make the most of your financial opportunities. Rather than taking a one-size-fits-all approach, it looks at your unique situation—your income, investments, goals, and timeline—to identify strategies that can reduce your overall tax burden. This may include thoughtful decisions around how you invest, when you realize gains, how you withdraw income in retirement, or whether strategies like Roth conversions make sense. By being proactive and intentional, a personalized tax plan helps ensure you’re not paying more than necessary and allows more of your money to stay invested and working toward your long-term goals.

What Tax Planning Includes

Clients working with Ascent Financial Group typically receive tax planning support that includes:

Year-round tax strategy coordination

Roth conversion planning

Tax-loss harvesting analysis

Tax-efficient income planning

Tax return review for planning insights

Coordination with investment and retirement strategy

Common Questions About Tax Planning

Can a financial advisor help with year-round tax planning?

Yes. A financial advisor can play a key role in tax planning throughout the year, not just at tax time. By reviewing your investments, income, and financial goals on an ongoing basis, an advisor can identify opportunities to reduce your tax liability—such as tax-loss harvesting, strategic account withdrawals, or timing income and deductions.

Year-round planning helps ensure your tax strategy is integrated with your broader financial plan, so you’re making decisions that optimize both your wealth and your long-term goals, rather than reacting to taxes only when filing season arrives.

How do Roth conversions fit into a tax strategy?

Roth conversions can be a powerful tool for managing taxes over the long term. By converting money from a traditional retirement account to a Roth account, you pay taxes on the amount converted today—but future earnings and withdrawals from the Roth grow tax-free.

When used strategically, Roth conversions can help manage your taxable income in retirement, reduce required minimum distributions (RMDs), and take advantage of lower tax brackets. The key is timing and scale: done thoughtfully, they can be an effective part of a broader tax and retirement plan to keep more of your wealth working for you.

How do I reduce taxes on equity compensation?

Equity compensation—like stock options, restricted stock units (RSUs), or employee stock purchase plans (ESPPs)—can create significant tax liability if not managed carefully. Strategies to reduce taxes include timing when you exercise or sell shares, spreading income across multiple years, and using tax-advantaged accounts when possible.

Working with a financial advisor can help you coordinate equity compensation decisions with your overall financial plan, including retirement, cash flow, and risk management. By planning ahead, you can optimize your gains while minimizing the taxes you owe.